Research Paper:

Pricing Cash-or-Nothing Binary Options with Two Underlying Assets Under Default Risk

Chieh-Wen Hsu†

School of Qiaoxing Economics and Management, Fujian Polytechnic Normal University

No.1 Campus New Village, Longjiang Street, Fuqing, Fujian 350300, China

†Corresponding author

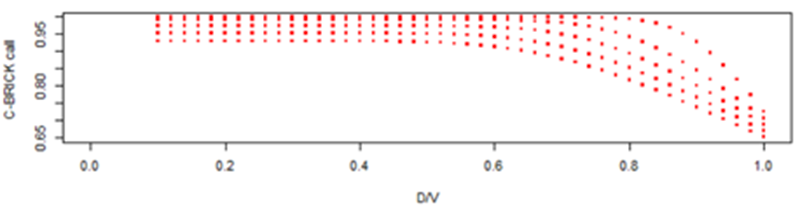

This study extended the theory of binary option pricing under default risk by extending the single underlying asset model to two underlying assets and a bilateral strike price model, while considering the correlation between different assets, focusing on the pricing analysis of cash-or-nothing binary options. The study derives a closed form options pricing formula using the Martingale method and proves that the formula is applicable to the pricing formula of binary option call and put options under default risk. Finally, numerical examples are used to analyze the characteristics and hedging value changes of binary options with two underlying assets under default risk. In addition, this study also highlights that under default risk, hedging with multiple underlying options is more difficult than general option hedging operations. This formula helps issuers to further understand the important basis for effective hedging in the issuance of multiple underlying commodities.

Binary options under default risk

- [1] A. Thavaneswaran, S. S. Appadoo, and J. Frank, “Binary option pricing using fuzzy numbers,” J. of Applied Mathematics Letters, Vol.26, No.1, pp. 65-72, 2013. https://doi.org/10.1016/j.aml.2012.03.034

- [2] X. Qin, X. Lin, and Q. Shang, “Fuzzy pricing of binary option based on the long memory property of financial markets,” J. Intelligent and Fuzzy Systems, Vol.38, No.4, pp. 4889-4900, 2020. https://doi.org/10.3233/JIFS-191551

- [3] Y. Lu and R. Song, “Pricing of a binary option under a mixed exponential jump diffusion model,” Mathematics, Vol.12, No.20, Article No.3233, 2024. https://doi.org/10.3390/math12203233

- [4] M. Yang and Y. Gao, “Pricing formulas of binary options in uncertain financial markets,” AIMS Mathematics, Vol.8, No.10, pp. 23336-23351, 2023. https://doi.org/10.3934/math.20231186

- [5] B. Liu, “Toward uncertain finance theory,” J. of Uncertainty Analysis and Application, Vol.1, Article No.1, 2013. https://doi.org/10.1186/2195-5468-1-1

- [6] H. Johnson and R. Stulz, “The pricing of options with default risk,” J. of Finance, Vol.42, No.2, pp. 267-280, 1987. https://doi.org/10.1111/j.1540-6261.1987.tb02567.x

- [7] P. Klein, “Pricing Black-Scholes options with correlated credit risk,” J. of Banking & Finance, Vol.20, No.7, pp. 1211-1229, 1996. https://doi.org/10.1016/0378-4266(95)00052-6

- [8] P. Klein and M. Inglis, “Valuation of European options subject to financial distress and interest rate risk,” The J. of Derivatives, Vol.6, No.3, pp. 44-56, 1999. https://doi.org/10.3905/jod.1999.319118

- [9] G. X. Liu, Q. X. Zhu, and Z. W. Yan, “The Martingale approach for vulnerable binary option pricing under stochastic interest rate,” Cogent Mathematics and Statistics, Vol.4, No.1, Article No.1340073, 2017. https://doi.org/10.1080/23311835.2017.1340073

- [10] R. A. Jarrow and S. M. Turnbull, “Pricing derivatives on financial securities subject to credit risk,” J. of Finance, Vol.50, No.1, pp. 53-85, 1995. https://doi.org/10.1111/j.1540-6261.1995.tb05167.x

- [11] R. A. Jarrow, D. Lando, and S. M. Turnbull, “A Markov model for the term structures of credit risk spreads,” The Review of Financial Studies, Vol.10, No.2, pp. 481-523, 1997. https://doi.org/10.1093/rfs/10.2.481

- [12] H. Niu, Y. Xing, and Y. Zhao, “Pricing vulnerable European options with dynamic correlation between market risk and credit risk,” J. of Management Science and Engineering, Vol.5, No.2, pp. 125-145, 2020. https://doi.org/10.1016/j.jmse.2020.03.001

- [13] J. C. Hull and A. White, “The impact of default risk on the options and other derivatives securities,” J. of Banking & Finance, Vol.19, No.2, pp. 299-322, 1995. https://doi.org/10.1016/0378-4266(94)00050-D

- [14] X. Wang, “Pricing vulnerable European option with stochastic volatility correlation,” Probability in the Engineering & Informational Sciences, Vol.32, No.1, pp. 67-95, 2018. https://doi.org/10.1017/S0269964816000425

- [15] Q. Zhou and X. Li, “Vulnerable European options pricing under uncertain volatility model,” J. of Inequalities and Applications, Article No.315, pp. 1-16, 2019. https://doi.org/10.1186/s13660-019-2266-5

- [16] Y. M. Shiu, P. L. Chou, and J. W. Sheu, “A closed-form approximation for valuing European basket warrants under credit risk and interest rate risk,” Quantitative Finance, Vol.13, No.8, pp. 1211-1223, 2013. http://doi.org/10.1080/14697688.2012.741693

- [17] X. Wang, “Pricing European basket warrants with default risk under stochastic volatility models,” Applied Economics Letters, Vol.29, No.3, pp. 253-260, 2022. https://doi.org/10.1080/13504851.2020.1862745

- [18] X. Wang, “Valuing vulnerable options with two underlying assets,” Applied Economics Letters, Vol.27, No.21, pp. 1699-1760, 2020. https://doi.org/10.1080/13504851.2020.1713980

This article is published under a Creative Commons Attribution-NoDerivatives 4.0 Internationa License.