Research Paper:

Impact of Management Risk Neglect on Export Sophistication: A Textual Analysis Perspective

Jiayu Gao, Fangting Yang†, and Wentao Gu

Department of Statistics, Zhejiang Gongshang University

No.18 Xuezheng Street, Xiasha Higher Education Park, Hangzhou, Zhejiang 310018, China

†Corresponding author

The 2008 global financial crisis significantly impacted Chinese export manufacturing firms. This study examines how management risk neglect affected these firms’ export sophistication during this period. Using panel data from 2006–2010, we treat the crisis as a natural experiment and quantify managerial risk neglect through natural language processing and sentiment analysis. Our intensity double-difference model reveals that firms with higher precrisis managerial risk neglect experienced steeper declines in export sophistication following the crisis. This suggests that risk neglect hinders firms’ strategic adjustments and export upgrading during external shocks. This finding remains robust across various tests. The negative effect was particularly pronounced among large firms, state-owned enterprises, and firms located on the east coast. Furthermore, greater financing constraints were found to mitigate the impact of managerial risk neglect on declining export sophistication. This research contributes to the managerial behavioral finance and export sophistication, offering practical guidance and policy recommendations for Chinese export manufacturing firms seeking to enhance their competitiveness in uncertain trade environments.

1. Literature Review

1.1. Export Sophistication

Export sophistication has become an important topic in international trade because it is a key measure of economic competitiveness. Research in this area generally follows two primary approaches: how to measure and what factors influence it. In terms of measurement methods, the discussion of measurement began with Michaely’s 1 trade specialization index. Hausmann et al. 2 built on this work by using their PRODY and EXPY indices. Koopman et al. 3 developed a global input-output model, allowing them to compute a revealed comparative advantage index using only the domestic value component, offering a more accurate view of a nation’s position in global value chains. There is a wealth of research on influencing factors at the macro level. Hausmann et al. 3 applied the EXPY index and found a strong relationship between a country’s export structure and its future economic growth.

1.2. Management Risk Neglects

The 2008 global financial crisis provided a critical opportunity to observe how risk perceptions influenced export behavior. The crisis, driven by vulnerabilities in the financial system and exacerbated by pro-cyclical leverage in cross-border bank balance sheets 4, shows that managerial risk neglect amplifies the impact on firms’ export activities 5. Early studies on risk neglect have focused on company performance and financial results. In their survey of over a hundred risk experts, Sjöberg et al. 6 highlighted that overlooked risks are marginalized owing to limited resources and social amplification or attenuation dynamics.

Although these studies offer a multidimensional view of management risk neglect, they lack a direct and detailed conceptualization of managers’ subjective cognitive processes 5,7. This study defines managerial risk neglect as corporate management’s tendency to systematically underestimate, downplay, or even actively ignore potential risks during strategic decision-making and information disclosure preparation processes. This definition emphasizes three points: first, this behavior is not a random oversight or information deficiency, but rather a recognizable cognitive bias; second, it stems from research in behavioral finance on decision-making under uncertainty; and third, its core manifestation involves the interaction of multiple biases, including overconfidence 8, confirmation bias 9, and optimism bias 10.

Current studies on management risk neglect exhibit a wide range of measurement methods; however, there is still great heterogeneity in the criteria in different contexts. International research has developed a more comprehensive standard for evaluating management risk neglect, including behavioral experiments, questionnaire surveys, and financial indicator analysis 11. Domestic scholars’ research on management risk neglect measurement presents theoretical perspectives and methodological features that differ from those of foreign countries. Deng et al. 12 used text analysis to extract sentiment data from annual reports and financial news and found a negative correlation between managerial risk neglect and sustainable development. Their conclusions show a negative correlation between risk neglect and sustainable development, thus providing a possible solution to the challenges facing the applicability of traditional measurement methods in the digital age. Unlike previous studies that measured management risk attitudes through indirect indicators, this study refers to the approach of Loughran and McDonald 13 and uses the definition of management risk neglect as its theoretical basis. It adopts an emotional quantification perspective and uses text analysis to directly measure the language and emotions of managers in annual reports and other documents.

1.3. Impact of Management Risk Neglect on Export Sophistication

Early behavioral finance theory linked the impact of management risk neglect on exports to cognitive bias 14. In the short run, risk underestimation leads to decision-making rigidity; financially vulnerable firms experience more severe export declines as a result of neglecting liquidity management 5, and such shocks dampen the margin of aggregation far more than the margin of expansion 15. However, in the long term, crises can have a pushback effect. Persistent external shocks often compel firms to reevaluate and address gaps in their risk perception 16. Simultaneously, firms that use trade credit as an alternative to bank financing demonstrate greater resilience 5. Most existing studies use financial indicators as indirect proxies to analyze management’s risk perception 7, which makes it difficult to provide in-depth insights into management’s subjective cognitive processes and has limitations at the analytical level.

2. Theoretical Analysis and Research Hypothesis

2.1. Management Risk Neglect and Export Sophistication: Based on Decision Process and Resource Allocation Perspectives

In times of heightened economic uncertainty, the risk perceptions and attitudes of a firm’s management have a significant impact on strategic choices and performance 17. Firms with higher levels of management risk neglect before a crisis experience a more significant decline in export sophistication after the crisis. This influence occurs via two main paths: cognitive bias and resource allocation.

First, according to prospect theory 18, managerial expectations in risky situations are often influenced by cognitive biases, particularly when managers are overconfident or risk neglecting 8. This bias prevents them from properly identifying and evaluating potential shocks, such as economic recessions or supply chain disruptions, and hinders their ability to invest strategically in export sophistication.

Second, at the strategic choice and resource allocation levels, the above cognitive bias directly led to the lagging of enterprises’ strategic layouts and resource mismatches before the crisis. Enhancing export sophistication requires firms to continuously invest large amounts of resources 2. However, managements with high-risk neglect and short-term focus tend to prioritize maintaining the current business model; when a financial crisis occurs, such firms struggle to survive, leading to a simpler export structure after the crisis 19.

-

H1:

Firms with higher precrisis management risk neglect experience a greater decline in export sophistication after a financial crisis.

2.2. Management Risk Neglect and Export Sophistication: A Firm Heterogeneity-Based Perspective

The effect of management risk neglect on export sophistication is not straightforward, but it is significantly moderated by firms’ characteristics.

First, the firm size is an important moderator. Large firms usually have stronger organizational inertia owing to their large and complex organizational structures, solidified decision-making processes, and highly specialized divisions of labor 20. When management neglects risk prior to a crisis, their over-optimism can create path dependence, solidify existing strategies, and reduce responsiveness to external changes 21, which can worsen the effects of risk neglect, making it more difficult to adapt once a crisis hits.

Second, ownership structure also plays a pivotal role. For instance, state-owned enterprises (SOEs) often face multiple, sometimes conflicting, policy objectives. They face less competitive pressure from the market, which may foster risk ignorance in their management 22. It has been suggested that the unique governance structure of SOEs may amplify the impact of management’s discretion and behavioral biases, leading to a greater negative effect on the adjustment of export sophistication during crisis 23. When a crisis occurs, their lower flexibility to adjust exacerbates their reactive response to external shocks, making reductions in export sophistication more pronounced.

Finally, geographical location influences firms’ integration into the global economy. Eastern seaboard firms, with a higher export share owing to their closer ties to global value chains, are more exposed to global shocks. In this environment of high-risk exposure, strategic vulnerability arising from management’s neglect of risk dramatically increases 24.

-

H2:

The negative impact of precrisis management risk neglect on export sophistication is more pronounced among large firms, SOEs, and firms located on the eastern seaboard.

2.3. Moderating Role of Financing Constraints

During a financial crisis, firms generally face a credit crunch and financing difficulties. Financing constraints, such as external market friction, undermine the role of management risk neglect in reducing firms’ export sophistication.

Firms face severe financing constraints due to the general tightening of external financing channels resulting from the sharp rise in market uncertainty and the impaired functioning of financial markets during a financial crisis 25,26. Finance availability is a fundamental prerequisite for increasing export sophistication 27. External financial constraints limit a firm’s ability to implement large-scale investments. Even if risk-neglectful managers remain optimistic about sustaining or expanding high-complexity production lines, a lack of financial support often prevents these plans from being executed 28. Consequently, limitations in external financing substantially reduce the sensitivity of firm investments to managerial sentiment during periods of uncertainty 29.

-

H3:

Higher financing constraints during financial crises weaken the role of managerial risk neglect in driving down firms’ export sophistication.

3. Data Selection and Study Design

3.1. Data Selection and Variable Definition

Listed export manufacturing companies were selected as the target of this study, and the study period spanned from 2006 to 2010. The enterprise-level data was gathered from the CSMAR database; the computation of export sophistication relied on the customs database, while the management risk oversight indicator was based on the textual information within annual reports. In this study, the data were processed as follows: (1) firms with ST, ST*, and PT status during the sample period were excluded; (2) firms listed after 2008 and firms that had already been delisted in 2008 were excluded; (3) firms with extensive missing data on key variables were excluded; and (4) the main continuous variables were subjected to a 1% reduction of tails. After screening, 511 firm-year observations for 103 firms were obtained.

3.2. Explanatory Variables: Export Sophistication

We draw on the ideas extended by Sheng and Mao 30 and Hausmann et al.’s 2 method. Specifically, the export sophistication of a single product is first calculated, and for the HS 6-digit code product, technical sophistication is given by

3.3. Core Explanatory Variables: Management Risk Neglect and Core Interaction Terms

This study defines management risk neglect as the management’s systematic underestimation of potential risks and excessive optimism. Considering the impact of management sentiment information contained in the tone and mood of financial texts on the market, this study adopts the Chinese sentiment lexicon in the financial field constructed by Yao et al. 31, which was developed through lexicon reorganization and deep learning algorithms and can be adapted to formal texts, such as annual reports, to quantitatively analyze the sentiment of annual report texts. Specifically, we quantify management’s emotional tendency in annual reports through a sentence-level sentiment scoring process and then construct annual management risk neglect indicators, which provide reliable support for the construction of indicators in this study.

(1) Text Preprocessing

The unstructured annual report text was preprocessed, including removing special characters and merging blank characters. The text was then segmented into independent sentences based on semantic meaning to form a sentence collection for sentiment analysis. Each sentence was then segmented and labeled with lexical properties using the Jieba lexical system.

(2) Sentiment Score

For each sentence, the sentiment score is calculated as follows:

(3) Contextual Analysis

To capture corporate sentiment more accurately, we further introduce contextual analysis. Referring to Vanzo et al. 32, a sliding window is used to consider the sentiment information of the sentences before and after the current sentence. The final sentiment score of each sentence (\(\mathit{Final{\_}Score}_{j}\)) is calculated by weighting the score of the current sentence by the average score of its context:

(4) Firm-Level Indicators

The final sentiment scores of all sentences in the text of the annual report are arithmetically averaged to obtain the firm’s sentiment index for the year; that is, management risk neglect.

The core explanatory variable is an interaction term that reflects the impact of prefinancial crisis management risk neglect on post-crisis firms’ export sophistication. First, the baseline state of precrisis management risk neglect is constructed. Specifically, this is the average of the firm’s management risk neglect indicator (\(\mathit{RiskNeglect}\)) from 2006–2007 (i.e., two years before the crisis). \(\mathit{Post}_{t}\) is a time dummy variable that defines the time boundaries of the financial crisis and is assigned a value of 1 in 2008 and the following years and 0 in the remaining years; that is, \(\mathit{Post}= 1\) (\(t>2008\)). The core interaction term, \(\mathit{RiskNeglect}_{\mathit{pre},i} \times \mathit{Post}_{t}\), represents the interaction between firms’ precrisis benchmarks of management risk neglect and the financial crisis.

Table 1. Definition of control variables.

3.4. Control Variables

Referring to Sheng and Mao 30, Zhong 34, and Su et al. 35, the control variables were listed in Table 1 alongside their definitions and calculation methods.

3.5. Study Design

This study employs an intensity double-difference model to explore the effect of management risk neglect on firms’ export sophistication before and after the 2008 financial crisis. The core model was set up as follows:

Here, \(\ln \mathit{ESI}_{it}\) is the explanatory variable representing the logarithm of firm \(i\)’s export technological complexity in year \(t\); \(\mathit{RiskNeglect}_{\mathit{pre},i} \times \mathit{Post}_{t}\) is the core explanatory variable, which is the interaction term between firm \(i\)’s pre-crisis management risk neglect benchmark and the financial crisis dummy variable; \(X_{\mathit{kit}}\) represents the set of control variables; \(\delta_{i}\) denotes the firm fixed effect; \(\lambda_{t}\) denotes the year (time) fixed effect; and \(\varepsilon_{it}\) is the residual term. The coefficient of the interaction term, \(\beta_{1}\), captures the effect of the level of pre-crisis management risk neglect on the magnitude of change in firms’ export sophistication before and after the crisis.

4. Empirical Results and Analysis

4.1. Analysis of Baseline Regression Results

We use a continuous difference-in-differences (DID) model to assess the impact of managerial risk neglect on export sophistication during the 2008 financial crisis. The results of the benchmark regression are presented in Table 2 using two standard error estimation methods: robust estimation and bootstrap estimation. We find that the interaction term coefficient (\(\mathit{RiskNeglect}_{\mathit{pre},i} \times \mathit{Post}_{t}\)) is significantly negative in all regressions, and these negative coefficients remain significant when robust standard errors are used (columns (1) and (2)), regardless of whether control variables are included. When using the bootstrap approach (columns (3) and (4)), the inclusion of control variables not only preserved the results but also increased their statistical significance from the 5% level to the 1% level. Industry-level exogenous shocks are commonly used as instrumental variables to test the effectiveness of causal identification. However, the sample size of this study is limited, and the number of firms in each industry is small. Constructing this variable by industry would substantially reduce the number of available observations, weaken identification validity, and could produce a weak instrumental variable with not robust estimates; therefore, it is not included. In summary, these findings provide strong empirical support for hypothesis H1. They suggest that firms that managed higher risk before the financial crisis experienced a more significant decline in their export sophistication after the crisis.

Table 2. Baseline regression results.

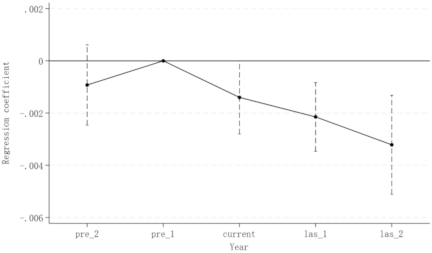

4.2. Parallel Trend Test

To verify the reasonableness of the model, we conducted a parallel trend and dynamic effect test, which is shown in the following equation:

Fig. 1. Parallel trend test.

Table 3. Robustness test.

Table 4. Post-PSM regression results.

4.3. Robustness Test

In this section, we focus on the robustness of the baseline regression results and further test them based on baseline regression model (2) through a variety of methods, such as placebo tests based on spurious years, substitution of explanatory variables, and construction of the PSM-DID model. Table 3 presents the robustness test results.

4.3.1. Placebo Test Based on Spurious Years

We conducted a placebo test to ensure that the results were not driven by unobservable confounding factors. This test artificially advanced the timing of the financial crisis by one year. The results in Table 3 indicate that the coefficient of this falsified interaction term was statistically insignificant. This result supports the robustness of the benchmark findings.

4.3.2. Replacing the Core Explanatory Variables

To further enhance the robustness of the findings and validate the impact of management risk neglect from another dimension of quantitative sentiment analysis, we introduce a positive-tone indicator (Tone) of corporate annual reports as a proxy measure of management risk neglect. This indicator aims to assess the degree of optimism or the signaling effect of management on corporate performance and market outlook in the text of annual reports; the higher the value, the more optimistic the management’s sentiment, which in turn reflects the higher degree of its potential risk neglect. As can be observed from the data in Table 3, the impact coefficient is \(-20.83\), and it is significant at the 1% level, suggesting that firms with higher precrisis management risk neglect still experience a significantly larger decline in export sophistication after the financial crisis, even when different methods of quantifying textual sentiment are used to measure management risk neglect. This finding is highly consistent with the benchmark regression results, which verify the robustness and reliability of hypothesis H1 from different perspectives.

Table 5. Heterogeneity tests and moderating effects.

4.3.3. Propensity Score Matching-Difference-in-Differences (PSM-DID)

Given that the points in time and firms affected by the 2008 financial crisis were not selected randomly, the model may suffer from selection bias, which may lead to a correlation between the explanatory variables and residuals, thus triggering endogeneity issues. Therefore, propensity score matching was necessary to ensure the robustness of the findings. In this study, the mean value of the precrisis management risk-neglect indicator (\(\mathit{RiskNeglect}\)) was used to divide the treatment group (high-risk neglect firms) and control group (low-risk neglect firms). To avoid the loss of information caused by the failure of matching too many samples, we used \(1:4\) nearest-neighbor matching, kernel matching, radius matching, and key continuous covariate-based Mahalanobis distance matching to develop a regression analysis on the matched samples. As shown in Table 4, the results indicate that the coefficients of the core interaction terms remain significantly negative across all four matching methods, indicating that the 2008 financial crisis prompted a greater decline in export sophistication among firms with higher precrisis management risk neglect, thereby confirming the robustness of the estimation results.

4.4. Heterogeneity Analysis

4.4.1. Firm Size Heterogeneity

First, we examine the heterogeneity across firm sizes by splitting the median sample into large and small firm subsamples. The results from our benchmark model, presented in Columns (1) and (2) of Table 5, indicate that the effect is concentrated in larger firms. For this group, the coefficient of the core interaction term (\(\mathit{RiskNeglect}_{\mathit{pre},i} \times \mathit{Post}_{t}\)) is \(-0.0034\) and is highly significant (\(p < 0.001\)), whereas the corresponding coefficient for small firms (\(-0.0010\)) is statistically insignificant, suggesting that the difference in the change in export sophistication due to the financial crisis shock is mainly reflected in large firms, thus validating part of hypothesis H2. Owing to their inherent organizational inertia, large firms further amplify negative shocks through their sluggishness in strategic adjustments when management risk neglect is higher before the crisis, leading to a more dramatic decline in export sophistication.

4.4.2. Enterprise Nature Heterogeneity

Next, samples of enterprise nature, state-owned and private enterprises, are selected to empirically test the difference in the impact of management risk neglect on export sophistication before and after the financial crisis. The regression results are presented in Columns (3) and (4) of Table 5, where the coefficient of the core interaction term of SOEs is \(-0.0022\) (\(p < 0.01\)), which is significantly lower than that of private enterprises (\(-0.0016\), not significant). This finding indicates that the negative effect of management risk neglect under a financial crisis shock is more significant for SOEs. The unique nature of property rights and the governance structure of SOEs may lead to the negative effect of management risk neglect being more difficult to curb, thus making the decline in their export sophistication more prominent, which also supports hypothesis H2.

4.4.3. Geographic Region Heterogeneity

Finally, the sample was divided by geographic region, and enterprises were divided into eastern and non-eastern coastal enterprises to examine the regional economic structure on the effect of management risk, neglecting the heterogeneity effect. The regression results are presented in Columns (5) and (6) of Table 5, where the coefficient of the core interaction term for eastern coastal firms is \(-0.0026\) (\(p < 0.001\)), while the coefficient for non-eastern coastal firms is 0.0010 (not significant). This suggests that in the post-financial crisis period, higher precrisis management risk neglect significantly dampens the enhancement of export sophistication among export-oriented eastern seaboard firms. The high degree of internationalization and deep integration into global value chains among eastern coastal firms cause them to suffer from greater export sophistication shocks under management risk neglect, further supporting hypothesis H2.

4.5. Moderating Effect Analysis

To examine the role of financing constraints in the relationship between firms’ precrisis sentiment benchmarks and post-crisis changes in export sophistication, we constructed a moderated effects model that includes an interaction term between financing constraints (\(\mathit{FC}\)) and the core explanatory variables (\(\mathit{RiskNeglect}_{\mathit{pre},i} \times \mathit{Post}_{t}\)). Drawing on the existing literature that analyzes the impact of the external financing environment on firms’ responses to external shocks 36,37, we theorize that financing constraints may limit the ability of firms to translate expectations reflected in sentiment into actual strategic adjustments. The regression model setup is similar to that of benchmark model (2), with the addition of the financing constraint variable and its interaction term with the core interaction term:

Column (8) of Table 5 indicates that the coefficient of the key moderator term, \(\mathit{RiskNeglect}_{\mathit{pre},i} \times \mathit{Post}_{t} \times \mathit{FC}_{it}\), is 0.0048 and significant at the 5% statistical level. This finding indicates that financing constraints have a significant positive moderating effect on the negative relationship between precrisis management risk neglect and post-crisis changes in export sophistication. Since the main effect coefficient of the core interaction term \(\mathit{RiskNeglect}_{\mathit{pre},i} \times \mathit{Post}_{t}\) is negative and the moderator coefficient is positive, this implies that the higher the level of financing constraints, the weaker the negative effect of management risk neglect on the decline in firms’ export sophistication.

Our findings strongly support H3: Financing constraints dampen the negative effects of management risk neglect. During a crisis, tight credit acts as a hard budget constraint, limiting the poor choices that biased managers may otherwise make. For instance, managers prone to risk neglect may resist reducing losses in a failing export venture. However, a lack of funds prevents them from returning to such inefficient operations. Thus, external discipline from capital markets curbs the real-world damage caused by managerial overoptimism. Therefore, the harm from risk neglect is less severe in firms with tighter financial constraints because their ability to make costly mistakes is lower.

5. Conclusion and Policy Recommendations

We quantitatively identify the level of management risk neglect based on panel data of Chinese listed export manufacturing firms from 2006 to 2010 by innovatively applying natural language processing and text analysis methods. By considering the 2008 global financial crisis as an exogenous shock, we examine in-depth the impact mechanism of precrisis management risk neglect on firms’ export sophistication, and the results of the study indicate that:

The 2008 financial crisis had a significant negative shock on listed export manufacturing firms with higher levels of precrisis management risk neglect, leading to a greater decline in export sophistication. This core finding, which suggests that management risk neglect hinders firms’ strategic adjustments and export structure upgrades in the face of external shocks, remains significant after conducting multiple robustness tests. Further research reveals that this negative effect varies by firm type. Specifically, the negative effect of precrisis management risk on the decline in export sophistication is particularly significant among large firms, SOEs, and eastern coastal firms. Our analysis reveals the significant moderating effect of financing constraints. We find that for firms facing tighter credit conditions, the damaging influence of management risk neglect on their export sophistication is substantially reduced.

Based on the above findings, we propose the following policy recommendations to encourage Chinese export manufacturing firms to enhance their export competitiveness in an uncertain trade environment.

First, the government should guide enterprises to improve their ability to identify, assess, and respond to global economic uncertainty and potential risks by improving information disclosure, promoting risk management best practices, and providing relevant training and consulting services. In particular, more targeted policy tools can be designed for large firms, SOEs, and eastern seaboard firms to incentivize them to establish sound internal risk control systems and flexible strategic adjustment mechanisms to effectively counteract the negative impact of external shocks on export sophistication. Second, given the moderating role of financing constraints on the risk-neglecting effects of management, the government should continue to deepen financial reforms and optimize the financial service system to ensure that export-oriented manufacturing firms have access to adequate and reasonably costly financial support in the face of external shocks. This includes encouraging financial institutions to innovate financial products, expanding enterprise financing channels, and lowering financing costs to provide enterprises with sufficient resources for strategic inputs such as technological innovation, product structure optimization, and international market diversification, and to turn external challenges into opportunities to enhance their export competitiveness.

- [1] M. Michaely, “Trade, Income Levels, and Dependence,” North-Holland, 1984.

- [2] R. Hausmann, J. Hwang, and D. Rodrik, “What you export matters,” J. of Economic Growth, Vol.12, No.1, pp. 1-25, 2007. https://doi.org/10.1007/s10887-006-9009-4

- [3] R. Koopman, W. Powers, Z. Wang, and S.-J. Wei, “Give credit where credit is due: Tracing value added in global production chains,” NBER Working Paper, No.16426, 2010. https://doi.org/10.3386/w16426

- [4] J. Pedrono, “The currency channel of the global bank leverage cycle,” J. of Int. Money and Finance, Vol.126, Article No.102652, 2022. https://doi.org/10.1016/j.jimonfin.2022.102652

- [5] B. Coulibaly, H. Sapriza, and A. Zlate, “Financial frictions, trade credit, and the 2008–09 global financial crisis,” Int. Review of Economics & Finance, Vol.26, pp. 25-38, 2013. https://doi.org/10.1016/j.iref.2012.08.006

- [6] L. Sjöberg, M. Peterson, J. Fromm, Å. Boholm, and S.-O. Hanson, “Neglected and overemphasized risks: The opinions of risk professionals,” J. of Risk Research, Vol.8, Nos.7-8, pp. 599-616, 2005.

- [7] M. Amiti and D. E. Weinstein, “Exports and financial shocks,” NBER Working Paper Series, No.15556, 2009.

- [8] U. Malmendier and G. Tate, “CEO overconfidence and corporate investment,” The J. of Finance, Vol.60, No.6, pp. 2661-2700, 2005. https://doi.org/10.1111/j.1540-6261.2005.00813.x

- [9] R. S. Nickerson, “Confirmation bias: A ubiquitous phenomenon in many guises,” Review of General Psychology, Vol.2, No.2, pp. 175-220, 1998. https://doi.org/10.1037/1089-2680.2.2.175

- [10] T. Sharot, “The optimism bias,” Current Biology, Vol.21, No.23, pp. R941-R945, 2011. https://doi.org/10.1016/j.cub.2011.10.030

- [11] S. Sugianto, H. Hasriani, and R. M. Noor, “Innovations in risk measurement and management for strategic financing decisions,” Advances in Management & Financial Reporting, Vol.2, No.2, pp. 59-71, 2024. https://doi.org/10.60079/amfr.v2i2.263

- [12] G. Deng, H. Liu, J. Yan, and S. Ma, “Managing for the future: Managerial short-termism impact on corporate ESG performance in China,” The European J. of Finance, Vol.31, No.2, pp. 147-173, 2025. https://doi.org/10.1080/1351847X.2024.2387622

- [13] T. Loughran and B. McDonald, “When is a liability not a liability? Textual analysis, dictionaries, and 10-Ks,” The J. of Finance, Vol.66, No.1, pp. 35-65, 2011. https://doi.org/10.1111/j.1540-6261.2010.01625.x

- [14] D. Kahneman and S. Frueh, “Try to design an approach to making a judgment; Don’t just go into it trusting your intuition,” Issues in Science and Technology, Vol.38, No.3, pp. 23-26, 2022.

- [15] H. Görg and M.-E. Spaliara, “Exporters in the financial crisis,” National Institute Economic Review, Vol.228, pp. R49-57, 2014. https://doi.org/10.1177/002795011422800105

- [16] P. Eppinger and M. Smolka, “Firm exports, foreign ownership, and the global financial crisis,” CESifo Working Paper, No.8808, 2020. https://doi.org/10.2139/ssrn.3765306

- [17] M. Baker, J. Wurgler, and Y. Yuan, “Global, local, and contagious investor sentiment,” J. of Financial Economics, Vol.104, No.2, pp. 272-287, 2012. https://doi.org/10.1016/j.jfineco.2011.11.002

- [18] D. Kahneman and A. Tversky, “Prospect theory: An analysis of decision under risk,” Econometrica, Vol.47, No.2, pp. 263-292, 1979. https://doi.org/10.2307/1914185

- [19] K. Mellahi and A. Wilkinson, “Organizational failure: A critique of recent research and a proposed integrative framework,” Int. J. of Management Reviews, Vols.5-6, No.1, pp. 21-41, 2004. https://doi.org/10.1111/j.1460-8545.2004.00095.x

- [20] M. T. Hannan and J. Freeman, “Structural inertia and organizational change,” American Sociological Review, Vol.49, No.2, pp. 149-164, 1984. https://doi.org/10.2307/2095567

- [21] D. Miller and M.-J. Chen, “Sources and consequences of competitive inertia: A study of the U.S. airline industry,” Administrative Science Quarterly, Vol.39, No.1, pp. 1-23, 1994. https://doi.org/10.2307/2393492

- [22] A. Shleifer and R. W. Vishny, “Politicians and firms,” The Quarterly J. of Economics, Vol.109, No.4, pp. 995-1025, 1994. https://doi.org/10.2307/2118354

- [23] D. J. Denis, D. K. Denis, and A. Sarin, “Agency problems, equity ownership, and corporate diversification,” The J. of Finance, Vol.52, No.1, pp. 135-160, 1997. https://doi.org/10.2307/2329559

- [24] A. B. Bernard, J. B. Jensen, S. J. Redding, and P. K. Schott, “Firms in international trade,” J. of Economic Perspectives, Vol.21, No.3, pp. 105-130, 2007. https://doi.org/10.1257/jep.21.3.105

- [25] H. Almeida, M. Campello, and M. S. Weisbach, “The cash flow sensitivity of cash,” The J. of Finance, Vol.59, No.4, pp. 1777-1804, 2004. https://doi.org/10.1111/j.1540-6261.2004.00679.x

- [26] M. Campello, J. R. Graham, and C. R. Harvey, “The real effects of financial constraints: Evidence from a financial crisis,” J. of Financial Economics, Vol.97, No.3, pp. 470-487, 2010. https://doi.org/10.1016/j.jfineco.2010.02.009

- [27] S. M. Fazzari, R. G. Hubbard, B. C. Petersen, A. S. Blinder, and J. M. Poterba, “Financing constraints and corporate investment,” Brookings Papers on Economic Activity, Vol.1988, No.1, pp. 141-206, 1988. https://doi.org/10.2307/2534426

- [28] C. J. Hadlock and J. R. Pierce, “New evidence on measuring financial constraints: Moving beyond the KZ index,” The Review of Financial Studies, Vol.23, No.5, pp. 1909-1940, 2010. https://doi.org/10.1093/rfs/hhq009

- [29] S. N. Kaplan and L. Zingales, “Do investment-cash flow sensitivities provide useful measures of financing constraints?,” The Quarterly J. of Economics, Vol.112, No.1, pp. 169-215, 1997.

- [30] B. Sheng and Q. L. Mao, “Does import trade liberalization affect Chinese manufacturing export technological sophistication,?” The J. of World Economy, Vol.40, No.1, pp. 52-75, 2017 (in Chinese). https://doi.org/10.19985/j.cnki.cassjwe.2017.12.004

- [31] J.-Q. Yao, X. Feng, Z.-J. Wang, R.-R. Ji, and W. Zhang, “Tone, sentiment and market impacts: The construction of Chinese sentiment dictionary in finance,” J. of Management Sciences in China, Vol.24, No.5, pp. 26-46, 2021 (in Chinese). https://doi.org/10.19920/j.cnki.jmsc.2021.05.002

- [32] A. Vanzo, D. Croce, and R. Basili, “A context-based model for Sentiment Analysis in Twitter,” Proc. of COLING 2014, the 25th Int. Conf. on Computational Linguistics: Technical Papers, pp. 2345-2354, 2014.

- [33] L. Zhang, S. Wang, and B. Liu, “Deep learning for sentiment analysis: A survey,” WIREs Data Mining and Knowledge Discovery, Vol.8, No.4, Article No.e1253, 2018. https://doi.org/10.1002/widm.1253

- [34] W.-J. Zhong, “Trade facilitation and firm export technological sophistication: Micro-evidence from listed companies,” Modern Management Science, Vol.2024, No.3, pp. 139-147, 2024 (in Chinese).

- [35] C.-C. Su, Y.-Q. Zhang, and F. Wang, “The impact of green manufacturing on firm export technological sophistication: A quasi-natural experiment based on China’s green factory initiative,” Prices Monthly, Vol.25, No.1, pp. 73-82, 2025 (in Chinese). https://doi.org/10.14076/j.issn.1006-2025.2025.01.08

- [36] H. Almeida, M. Campello, and C. Liu, “The financial accelerator: Evidence from international housing markets,” Review of Finance, Vol.10, No.3, pp. 321-352, 2006. https://doi.org/10.1007/s10679-006-9004-9

- [37] A. Guariglia, “Internal financial constraints, external financial constraints, and investment choice: Evidence from a panel of UK firms,” J. of Banking & Finance, Vol.32, No.9, pp. 1795-1809, 2008. https://doi.org/10.1016/j.jbankfin.2007.12.008

This article is published under a Creative Commons Attribution-NoDerivatives 4.0 Internationa License.